Every wave of financial automation has promised broadly the same outcome: less paper, fewer errors, more time for the work that requires a human brain. The first wave digitised documents. The second moved everything into SaaS, then bolted on OCR, workflow engines and a layer of RPA bots held together by goodwill and Excel. None of it was wrong, it just left the hardest part of the job untouched: the chain of work between systems, where most of an administrator's day actually lives.

AI agents shift the picture in a way regulated firms should care about. They read messy documents, retrieve data, use the tools already on someone's desk, follow written policy, escalate the unusual, and, the part previous waves never quite managed, leave behind the audit trail that makes any of it defensible after the fact.

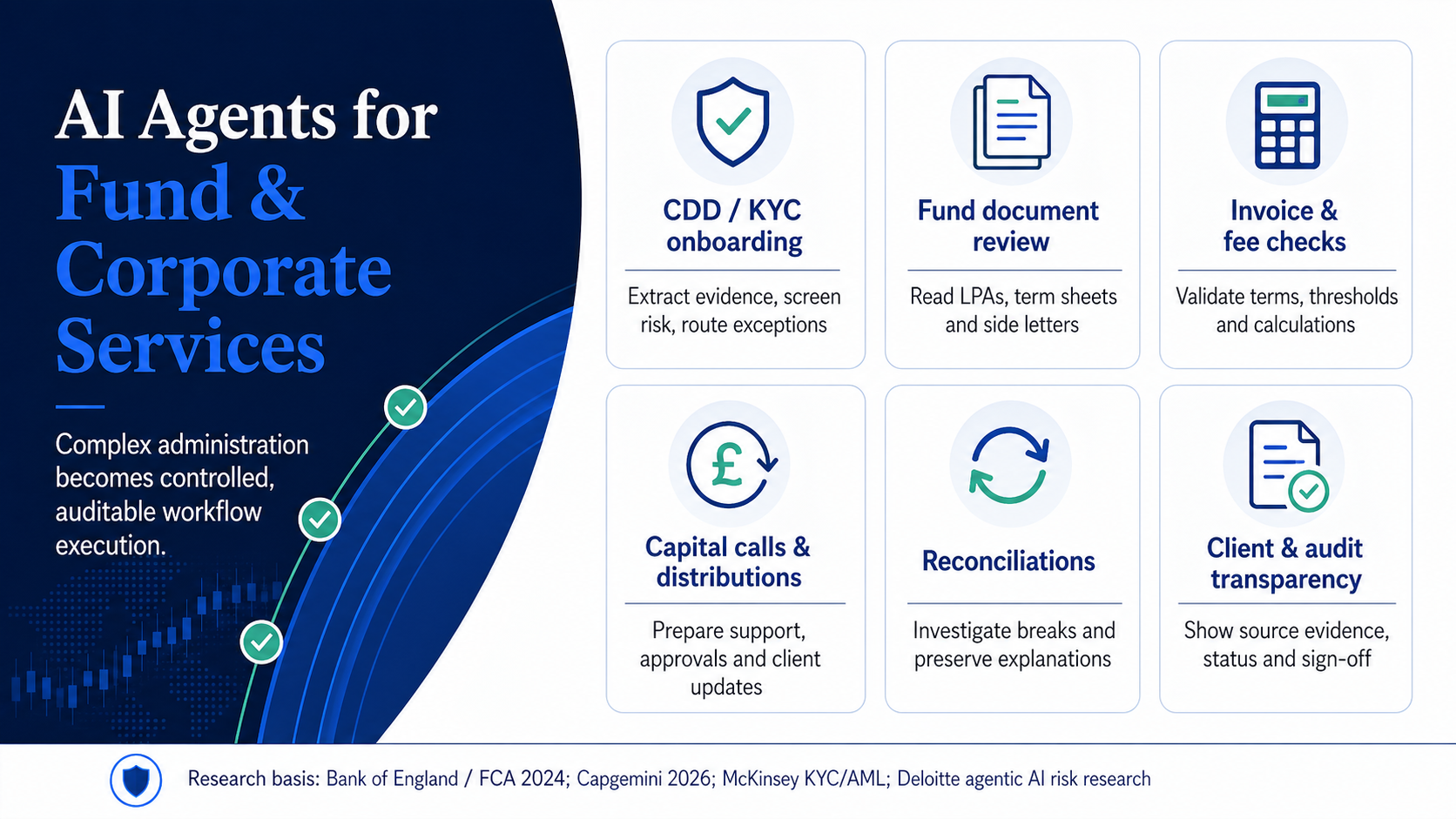

The hardest work in financial administration is rarely one clean task in one clean system. It's onboarding a new investor, walking through CDD and KYC evidence, checking fee terms against a side letter, reconciling records, prepping capital-call support, reviewing invoices, and answering an auditor who wants to know what was checked, when, and by whom. That's the territory CoreAdmin AI was built for. Financial administration for workflows where speed, control and transparency all have to hold at once.

Why regulated workflows resist standard automation

Financial administration looks repetitive from the road, but up close it's anything but. One fund's fee language isn't the next fund's. One investor file has missing evidence. An invoice references a side letter the previous administrator never saw, a capital call hangs on something agreed over email three years ago. A KYC review needs company registry data, ownership unwinding, PEP and sanctions screening, adverse media checks, a documented purpose of relationship, and at least one human signature on the way out. Multiply that by a few hundred investors and the variation that used to be a feature of bespoke service becomes the structural cost of running the business.

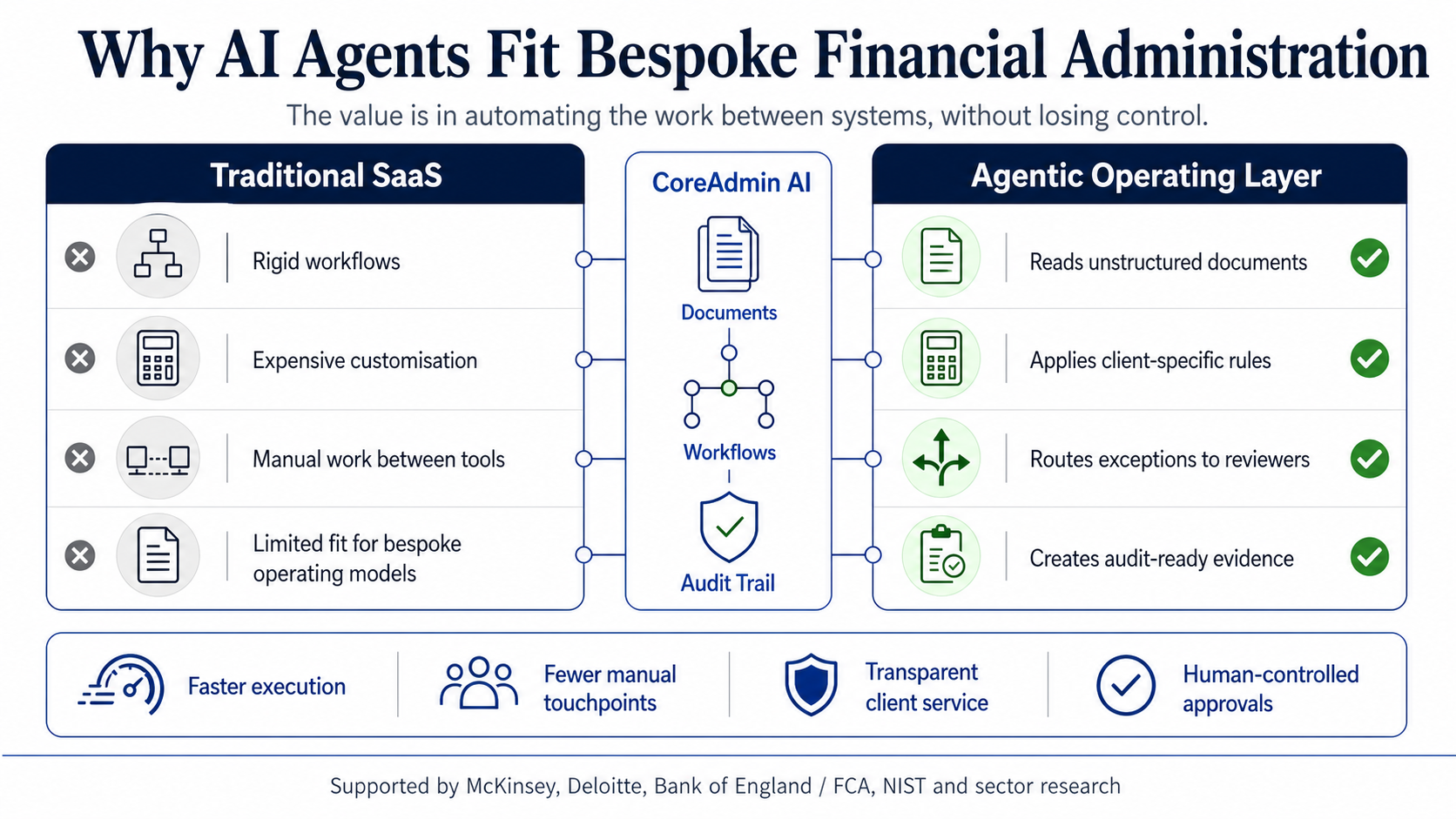

Traditional SaaS handles the standardised middle of the bell curve well enough. It struggles at the tails: the unusual side letter, the obscure tax wrapper, the legacy spreadsheet one director still treats as authoritative. The result, in most administrators we've seen up close, is a stack of disconnected systems, hand-typed reconciliations and a quiet but expensive layer of manual review that nobody's quite worked out how to get rid of.

"Rules-based automation is brittle when workflows have unexpected inputs, multiple possible outcomes and judgement-heavy exceptions. Agentic systems are more adaptable because they interpret natural-language instructions, work with the software already deployed, and handle the less predictable paths through a process."

McKinsey makes the same point with less mercy. Rules-based automation is brittle when workflows have unexpected inputs, multiple possible outcomes and judgement-heavy exceptions. Agentic systems are more adaptable because they interpret natural-language instructions, work with the software already deployed, and handle the less predictable paths through a process.1

That's the shift in economics. An administrator no longer has to choose between preserving its bespoke operating model and getting modern automation. An agentic layer can work across the systems and documents already in use, including, charitably, the spreadsheets nobody admits to.

The market has stopped pretending this is experimental

The supervisors' figures put the timeline on the table. The Bank of England and FCA's 2024 survey found 75% of responding UK financial services firms already using AI, with another 10% planning to within three years. The largest cluster of use cases are sitting in operations and IT, the back office, and the median number of use cases was expected to more than double over the following three years.2

Capgemini's World Cloud Report for Financial Services 2026 reads like the same sentence continued. Banks are planning to deploy cloud-native AI agents at scale across customer service, fraud detection, loan processing and onboarding. The same report flags onboarding, KYC, loan processing, claims and underwriting as some of the sector's least efficient functions.3 The parts of finance that matter least to clients but most to margins are exactly where agentic AI is being pointed.

This isn't a chatbot story. It's a process-execution story, and the distinction matters.

Morgan Stanley is probably the most useful public reference point. Its AI @ Morgan Stanley Assistant has been adopted by more than 98% of advisor teams, lifting document access from around 20% to 80% by the firm's own measure.4 A companion tool, AI @ Morgan Stanley Debrief, drafts meeting notes, identifies action items, prepares follow-up emails for advisor review and writes back into Salesforce.5 BlackRock has gone further still. Its Aladdin Wealth platform produces AI Auto Commentary for Morgan Stanley advisors, weaving portfolio analytics, CIO market views and client preferences into a narrative the advisor can read in a meeting.6

Stand back from the detail and the pattern's straightforward. AI is being used to absorb administrative drag so that experienced people spend more of their day on the conversations and judgements that justify their fees.

Compliance is the design requirement, not the obstacle

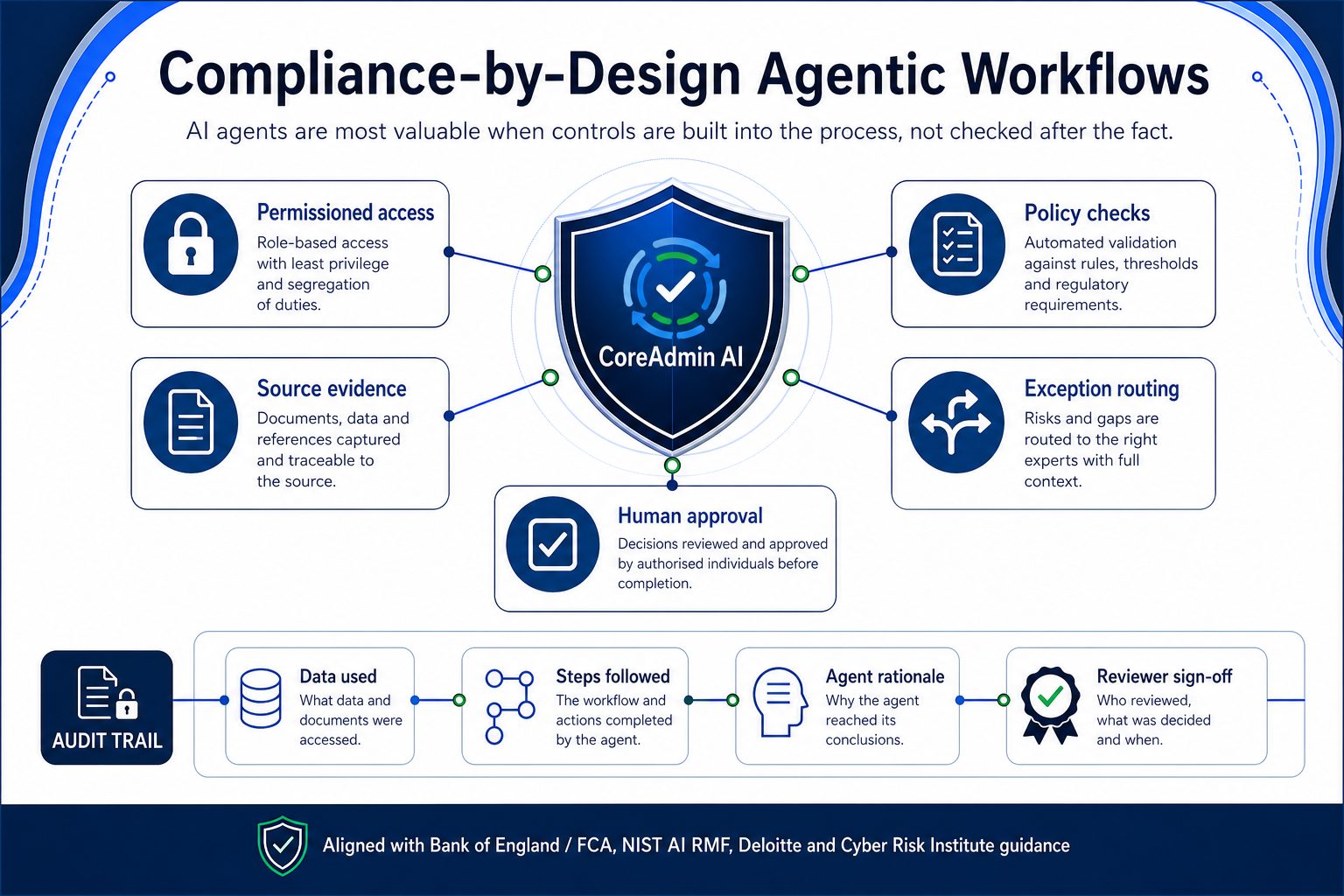

The strongest argument for AI agents in financial administration isn't raw efficiency. It's controlled transparency, and that's a less comfortable argument for vendors used to selling speed.

McKinsey's 2025 work on KYC and AML describes a global bank that built an agentic AI factory for end-to-end KYC. Specialist agent squads extracted client data, checked company registries, analysed ownership structures, identified beneficial owners, screened directors and UBOs, ran adverse media checks, and compiled a consolidated KYC file for human review. The most valuable output, by the bank's own assessment, wasn't the headline speed-up. It was the audit trail: the data used, the steps followed, the interactions between agents, the reasoning, and the QA observations.7

Regulatory context: The Bank of England and FCA survey finds firms cite data privacy, data quality and data security as their three largest current AI risks, while transparency and explainability remain among the binding constraints on adoption.2 Regulated firms don't need uncontrolled AI. They need AI built around permissions, traceability, governance and human oversight from the start.

That's the right direction for regulated operations. Every step evidenced, every exception visible, every recommendation reviewable. CoreAdmin AI sits in that category, not as a black-box replacement for professional judgement, but as an operating layer that reads, structures, checks, routes and evidences, and stops at the point where a person should decide.

Where the opportunity lives in financial administration

Financial administration is, in many ways, the textbook agentic AI use case:

- Document-heavy workflows: term sheets, LPAs, side letters, invoices, bank statements, onboarding packs, audit requests.

- Bespoke rules where fund documents, SLAs and internal controls determine the right answer, not a generic policy.

- Multi-system work stretched across email, document stores, accounting systems, CRMs, investor portals and the inevitable spreadsheet.

- Compliance-sensitive steps where the firm has to prove what was checked, when, by whom and on what evidence.

- Client-facing transparency where investors, managers and auditors expect clear status, clear rationale and the underlying records on demand.

CoreAdmin AI turns that surface area into controlled workflow execution. It pulls obligations and terms out of fund documents, validates fees, thresholds, dates and calculation logic against source evidence, routes exceptions to the right reviewer with context already attached, maintains an audit trail for each action and decision, and cuts back repetitive checking while leaving approvals and judgement calls firmly in human hands.

The six workflow areas where CoreAdmin AI agents operate, each one document-heavy, compliance-sensitive, and historically reliant on manual checking.

What that means in practice is faster administration without weakening oversight, historically the trade-off most firms have been unwilling to make, and rightly so.

Why this beats buying another SaaS

For a long time the default answer to an operational problem was a new SaaS subscription. It usually solved a narrow problem and left a wider mess behind: more logins, more integrations, more duplicated data, more renewals to negotiate, more permissions to manage, and more manual stitching between systems. Anyone who's tried to reconcile across three platforms at year-end will recognise the picture.

Agents change the cost model because they sit across existing tools rather than demanding to replace them. The agent reads the document, understands the task, retrieves the relevant data, applies the firm's policy, uses the correct downstream system, and prepares the output for review.

The early academic work points the same way. The FinRobot paper on generative business process agents in finance found that agent-based workflows could interpret user intent, synthesise workflows in real time and coordinate specialist sub-agents across tasks as varied as reporting and wire-transfer processing, with reported case-study improvements of up to a 40% reduction in processing time and a 94% drop in error rates.8

The lesson isn't that every workflow should be fully autonomous. It's that the expensive middle layer, the manual interpretation, checking, copying, reconciliation and evidence preparation that happens between systems, is finally a credible candidate for serious automation.

Agentic workflows, human controls

The future of regulated finance isn't "AI instead of controls." It's AI inside the controls.

Deloitte's recent work on finance and accounting professionals found trust is the leading barrier to agentic AI adoption, and that most respondents only trust agents to act inside a defined framework, with judgement calls reserved for people.9 That's not a position worth arguing with. It's the operating model.

Five principles, in our view, separate the firms that will get real value from agentic AI from those that'll quietly write off the budget:

- Human approval for material decisions. Always.No agent should settle, release or commit without a documented human sign-off at the threshold where it matters.

- Source evidence behind every output.Not just a confidently-worded answer, the document, field, version and timestamp that the answer came from.

- Permissioned access to systems and data.Scoped to the work in hand, not open-ended. Least-privilege by design.

- Audit trails by default, not as a feature flag for the auditors.Every action, every decision, every escalation, logged as standard operating behaviour.

- Exception-led workflows.Human expertise concentrates where it matters most, not on routine checking that a well-configured agent can handle.

That's how AI becomes commercially useful in financial administration. It doesn't ask firms to abandon judgement, compliance or bespoke processes. It gives teams a better operating layer for the work that currently disappears into inboxes, spreadsheets and unread review queues.

The bottom line

AI agents are becoming the new operating layer for complex financial processes. The interesting use cases aren't the generic chatbots that owned the headlines two years ago. They're controlled, auditable workflows that cut administrative burden, sharpen consistency and make process data genuinely transparent to clients, auditors and internal teams.

For fund administrators and regulated financial firms the opportunity is concrete: faster execution, less manual touchpoints, better evidence, clearer client service and stronger operational control, without trading any of those off against each other.

CoreAdmin AI is built for exactly that brief. Automation where it earns its keep. Human judgement where it should never have left.

Footnotes

- 1 McKinsey, Why agents are the next frontier of generative AI: agents handle variable workflows, natural-language instructions and existing software tools. mckinsey.com

- 2 Bank of England and FCA, Artificial Intelligence in UK Financial Services 2024: 75% of respondents already using AI; operations and IT is the largest use-case area; data privacy, quality and security are the leading risks. bankofengland.co.uk

- 3 Capgemini Research Institute, World Cloud Report, Financial Services 2026: banks deploying AI agents for customer service, fraud detection, loan processing and onboarding; only 10% have implemented at scale. capgemini.com

- 4 OpenAI and Morgan Stanley case study: more than 98% advisor-team adoption; document access increased from 20% to 80%; emphasis on evaluations and controls. openai.com

- 5 Morgan Stanley, AI @ Morgan Stanley Debrief launch: AI meeting notes, action items, draft follow-up emails and Salesforce notes with client consent and advisor review. morganstanley.com

- 6 BlackRock Aladdin Wealth and Morgan Stanley: AI Auto Commentary combines risk analytics, CIO market outlook and client portfolio preferences into advisor-ready narratives. blackrock.com

- 7 McKinsey, How agentic AI can change the way banks fight financial crime: agentic KYC/AML factory, human review, full audit trail, end-to-end process redesign. mckinsey.com

- 8 FinRobot research paper, Generative Business Process AI Agents for ERP in Finance: agent-based financial workflows, dynamic process synthesis, reported processing-time and error-rate improvements in case studies. arxiv.org/abs/2506.01423

- 9 Deloitte, Trust emerges as main barrier to agentic AI adoption in finance and accounting: agentic AI expected to become standard, but trust, controls and human judgement remain central. deloitte.com

Further reading on AI risk and governance

- Deloitte, Managing the new wave of risks from AI agents in banking

- NIST, AI Risk Management Framework

- Federal Reserve / OCC, SR 11-7 Model Risk Management

- Cyber Risk Institute, Financial Services AI Risk Management Framework

- World Economic Forum, Artificial Intelligence in Financial Services 2025

- Research paper, Agentic AI for Financial Crime Compliance